Walk through each Heston parameter in 1D first (rho for skew, xi for curvature, kappa for mean reversion, v_0 for level), then stack them into the full 3D implied vol surface and watch it morph when the starting variance shifts.

Black-Scholes assumes volatility is a constant. The market politely disagrees. Implied vol moves around every minute, the smile is asymmetric, and short-dated options price in a steeper skew than long-dated ones. None of that fits a single number.

The Heston model fixes the gap by letting variance itself be a stochastic process. The stock follows the usual lognormal dynamics, but the variance $v_t$ now has its own SDE with mean reversion and noise:

$$dS_t \;=\; r\,S_t\,dt \;+\; \sqrt{v_t}\,S_t\,dW_t^{(1)}$$

$$dv_t \;=\; \kappa(\theta - v_t)\,dt \;+\; \xi\,\sqrt{v_t}\,dW_t^{(2)}$$

$$\mathrm{corr}\,\!\bigl(dW^{(1)},\, dW^{(2)}\bigr) \;=\; \rho$$

That single change buys you four things Black-Scholes can't produce:

Five parameters, five things to think about: $\rho$, $\xi$, $\kappa$, $\theta$, $v_0$. The rest of this notebook is a 1D walk through each one, then the 3D surface, then a side-by-side of how the surface morphs when $v_0$ shifts from a low-vol to a high-vol regime.

Heston option prices aren't closed-form like Black-Scholes. The standard route is the characteristic function $\varphi(u)$ of $\log S_T$ — a complex-valued function we can integrate numerically (via Lewis-style Fourier inversion) to get the call price. We'll then invert that price into an implied vol with Brent's root finder against the Black-Scholes formula.

Three libraries: numpy for arrays, scipy for the integral

and the root finder, matplotlib for the plots.

pip install numpy scipy matplotlibImports + the characteristic function + the Heston call pricer + Black-Scholes inversion:

import numpy as np

from scipy.integrate import quad

from scipy.optimize import brentq

from scipy.stats import norm

# Defaults we will reuse below (equity-vol regime).

S0, R, Q = 100.0, 0.03, 0.00

V0, KAPPA = 0.019, 2.5

THETA, XI, RHO = 0.07, 0.75, -0.72

def heston_char(u, T, S0, r, q, v0, kappa, theta, xi, rho):

"""Albrecher 'little trap' form of the Heston characteristic function."""

u = np.asarray(u, dtype=complex)

xi_h = kappa - rho * xi * 1j * u

d = np.sqrt(xi_h**2 + xi**2 * (u * 1j + u**2))

g2 = (xi_h - d) / (xi_h + d)

C = (kappa * theta / xi**2) * (

(xi_h - d) * T - 2.0 * np.log((1 - g2 * np.exp(-d * T)) / (1 - g2))

)

D = ((xi_h - d) / xi**2) * (1 - np.exp(-d * T)) / (1 - g2 * np.exp(-d * T))

return np.exp(C + D * v0 + 1j * u * (np.log(S0) + (r - q) * T))

def heston_call(K, T, *, S0=S0, r=R, q=Q, v0=V0,

kappa=KAPPA, theta=THETA, xi=XI, rho=RHO):

"""Heston European call via Fourier-style numerical integration."""

args = dict(S0=S0, r=r, q=q, v0=v0, kappa=kappa, theta=theta, xi=xi, rho=rho)

def p1(u):

return np.real(np.exp(-1j*u*np.log(K)) * heston_char(u - 1j, T, **args)

/ (1j*u * heston_char(-1j, T, **args)))

def p2(u):

return np.real(np.exp(-1j*u*np.log(K)) * heston_char(u, T, **args) / (1j*u))

P1 = 0.5 + (1.0/np.pi) * quad(p1, 1e-8, 100, limit=200)[0]

P2 = 0.5 + (1.0/np.pi) * quad(p2, 1e-8, 100, limit=200)[0]

return S0 * np.exp(-q*T) * P1 - K * np.exp(-r*T) * P2

def bs_call(K, T, sigma, S0=S0, r=R, q=Q):

"""Black-Scholes call (used as the inversion target)."""

d1 = (np.log(S0/K) + (r - q + 0.5*sigma**2)*T) / (sigma*np.sqrt(T))

d2 = d1 - sigma*np.sqrt(T)

return S0*np.exp(-q*T)*norm.cdf(d1) - K*np.exp(-r*T)*norm.cdf(d2)

def implied_vol(price, K, T, S0=S0, r=R, q=Q):

"""Invert a call price to BS implied vol using Brent's method."""

intrinsic = max(S0*np.exp(-q*T) - K*np.exp(-r*T), 0.0)

if price <= intrinsic + 1e-8:

return np.nan

try:

return brentq(lambda s: bs_call(K, T, s, S0, r, q) - price, 1e-4, 5.0, xtol=1e-6)

except (ValueError, RuntimeError):

return np.nanBefore slicing the surface, a sanity check: what do these five parameters actually look like for real assets? The Heston model is calibrated to listed option prices, and the calibrated values differ wildly across asset classes. Equity indices, single names, bonds, gold, and crypto all live in very different corners of the parameter space.

The table below shows order-of-magnitude calibrated Heston parameters across five representative underlyings. Take it as a "feel for the numbers" rather than a quotation — actual calibrations depend on the date, the option chain you fit, and the moneyness window.

| Underlying | $\kappa$ (mean rev.) | $\theta$ (long-run var) | $\xi$ (vol of vol) | $\rho$ (skew) | $v_0$ (today) | Short-dated ATM vol |

|---|---|---|---|---|---|---|

| SPY (S&P 500) | 2.5 | 0.040 | 0.75 | −0.75 | 0.020 | ~14% |

| AAPL (single name) | 1.5 | 0.070 | 1.20 | −0.55 | 0.045 | ~21% |

| TLT (20+ yr Treasury) | 3.0 | 0.018 | 0.45 | +0.05 | 0.015 | ~12% |

| GLD (gold ETF) | 2.0 | 0.025 | 0.55 | −0.10 | 0.022 | ~15% |

| BTC (crypto, weekly) | 0.8 | 0.500 | 2.50 | −0.30 | 0.400 | ~63% |

Four patterns to read off the table:

One useful exercise once you have the code below working: plug in any row from this table and re-run the 1D slices. The smile under SPY parameters will look very different from the same smile under TLT or BTC. The rest of the notebook uses the SPY-style equity-vol regime as the default (matching the values printed in section 2), but every plotting cell takes keyword overrides so you can swap any subset of parameters in one line.

Before the 1D plots, a one-line summary of what each parameter does to the surface — so when you see the slices below, you already know which knob is being turned.

Now to the 1D slices. Each section below isolates one parameter, holds the others at the defaults, and walks the value across a sensible range so you can see its effect cleanly.

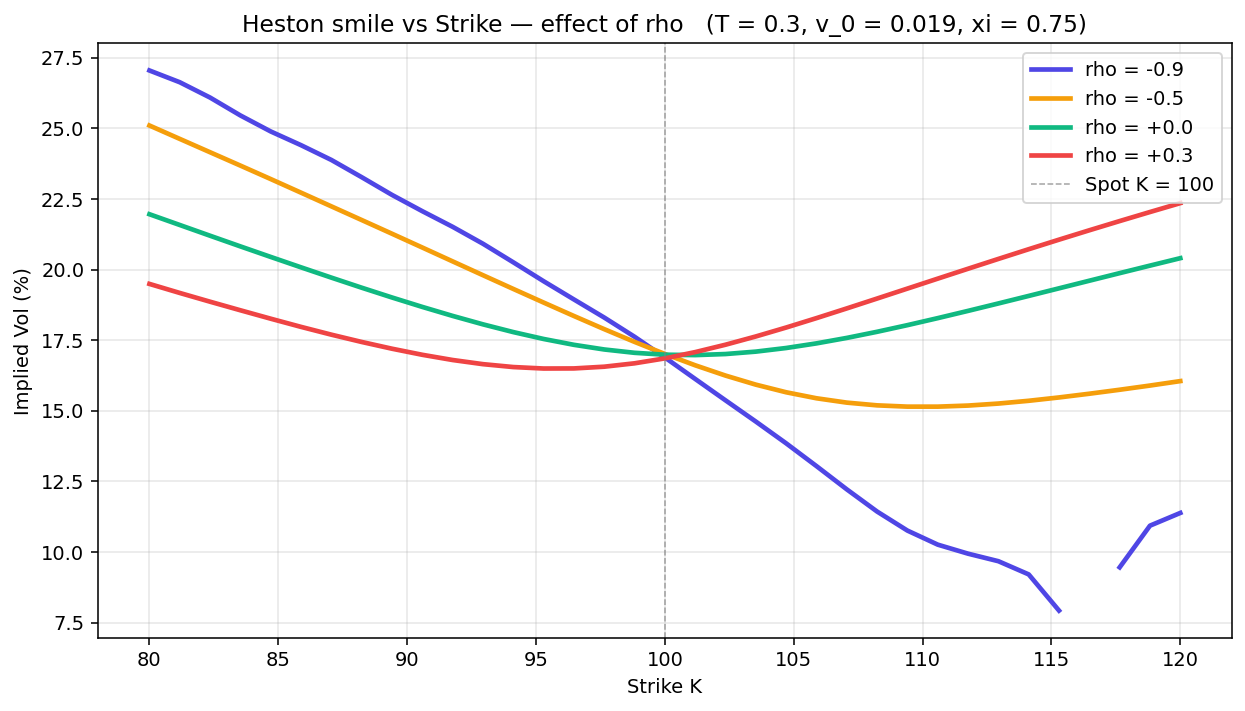

Fix everything else and only vary $\rho$. The smile tilts. $\rho < 0$ means a negative shock to the asset is correlated with a positive shock to its variance — the equity-vol "leverage effect". OTM puts price in higher vol than OTM calls, and the smile becomes a downward-sloping line of skew. As $\rho$ moves toward zero the smile becomes symmetric, and a positive $\rho$ flips the asymmetry the other way.

import matplotlib.pyplot as plt

T_fixed = 0.30

strikes = np.linspace(80, 120, 35)

plt.figure(figsize=(9, 5.2))

for rho_val in [-0.9, -0.5, 0.0, 0.3]:

ivs = [implied_vol(heston_call(K, T_fixed, rho=rho_val), K, T_fixed) for K in strikes]

plt.plot(strikes, np.array(ivs)*100, lw=2.4, label=f"rho = {rho_val:+.1f}")

plt.axvline(S0, color="gray", ls="--", lw=0.8, label=f"Spot K = {S0:.0f}")

plt.title(f"Heston smile vs Strike — effect of rho (T = {T_fixed}, v_0 = {V0}, xi = {XI})")

plt.xlabel("Strike K"); plt.ylabel("Implied Vol (%)")

plt.legend(); plt.grid(True); plt.tight_layout(); plt.show()

Pure rotation around the ATM strike. Strong negative $\rho$ (blue, $\rho = -0.9$) produces a deep left-skew — the equity vol leverage effect at full strength. Positive $\rho$ (red, $\rho = +0.3$) does the opposite. The deep-OTM noise on the $\rho = -0.9$ curve is the BS inversion hitting near-intrinsic prices, not a model error.

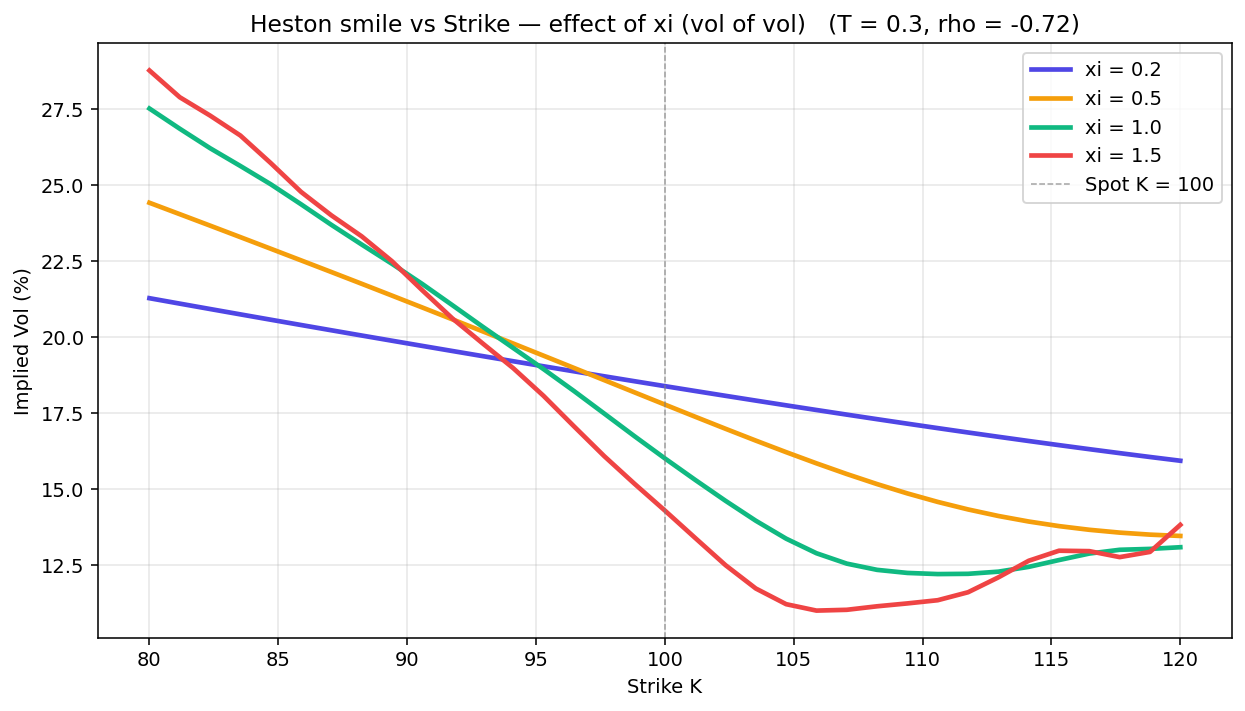

$\xi$ is the diffusion coefficient of the variance SDE. Intuitively: how violently variance kicks around. Higher $\xi$ means variance has a wider distribution at any future date, which fattens the tails of the implied $\log S_T$ distribution, which makes the smile more bowed. Low $\xi$ collapses the smile toward a flat Black-Scholes line.

plt.figure(figsize=(9, 5.2))

for xi_val in [0.2, 0.5, 1.0, 1.5]:

ivs = [implied_vol(heston_call(K, T_fixed, xi=xi_val), K, T_fixed) for K in strikes]

plt.plot(strikes, np.array(ivs)*100, lw=2.4, label=f"xi = {xi_val}")

plt.axvline(S0, color="gray", ls="--", lw=0.8, label=f"Spot K = {S0:.0f}")

plt.title(f"Heston smile vs Strike — effect of xi (vol of vol) (T = {T_fixed}, rho = {RHO})")

plt.xlabel("Strike K"); plt.ylabel("Implied Vol (%)")

plt.legend(); plt.grid(True); plt.tight_layout(); plt.show()

Same midpoint, different wings. As $\xi$ grows the smile bows out — the wings demand a higher vol because variance can wander further by expiry. $\rho$ controls the left-right tilt, $\xi$ controls how much the wings lift up.

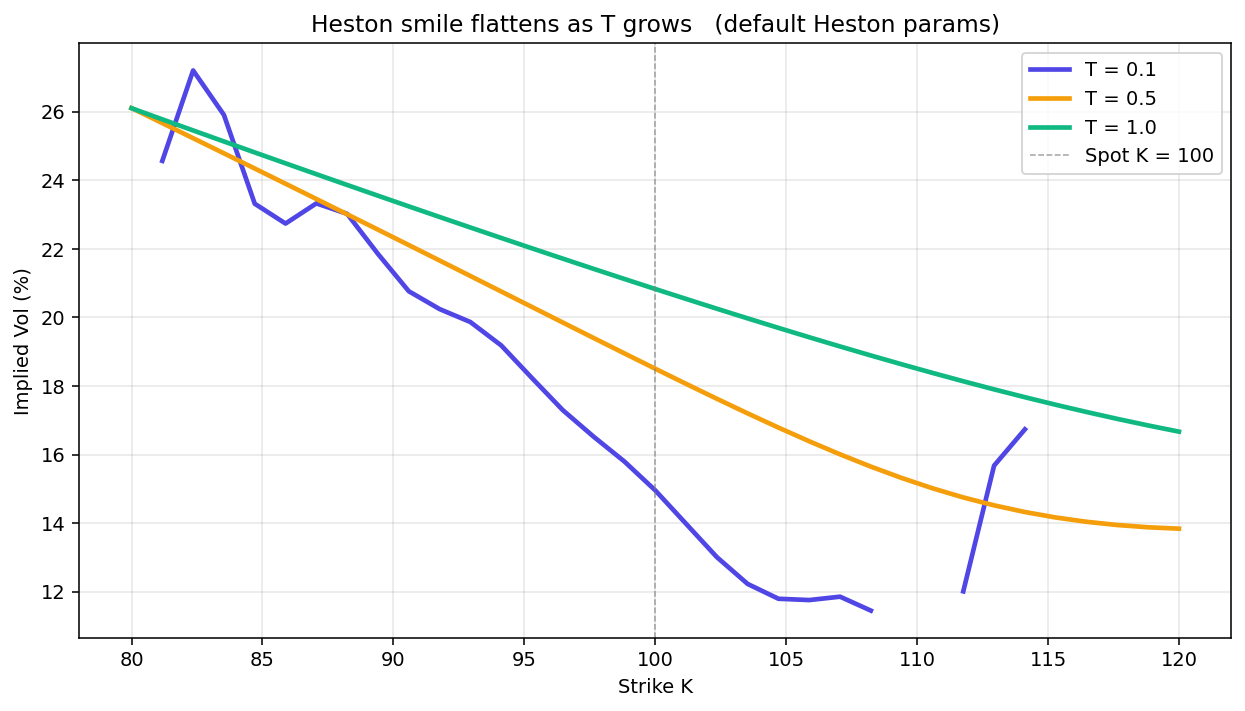

Keep all parameters at their defaults and walk the maturity instead. At short $T$, the variance hasn't had time to mean-revert, so the smile is steep and reflects all of $v_t$'s current asymmetry. At long $T$, the model averages over many possible variance paths and the smile flattens toward the long-run vol $\sqrt{\theta}$.

This is the single biggest reason BS doesn't fit real markets: the empirically observed flattening of the smile with $T$ is a stochastic-vol phenomenon, not a BS one.

plt.figure(figsize=(9, 5.2))

for T_val in [0.10, 0.50, 1.00]:

ivs = [implied_vol(heston_call(K, T_val), K, T_val) for K in strikes]

plt.plot(strikes, np.array(ivs)*100, lw=2.4, label=f"T = {T_val}")

plt.axvline(S0, color="gray", ls="--", lw=0.8, label=f"Spot K = {S0:.0f}")

plt.title("Heston smile flattens as T grows (default Heston params)")

plt.xlabel("Strike K"); plt.ylabel("Implied Vol (%)")

plt.legend(); plt.grid(True); plt.tight_layout(); plt.show()

$T = 0.10$ gives the steepest, most asymmetric smile. By $T = 1.0$ the smile is noticeably flatter and the level is closer to $\sqrt{\theta}$. This is what "stochastic vol generalises Black-Scholes" actually looks like.

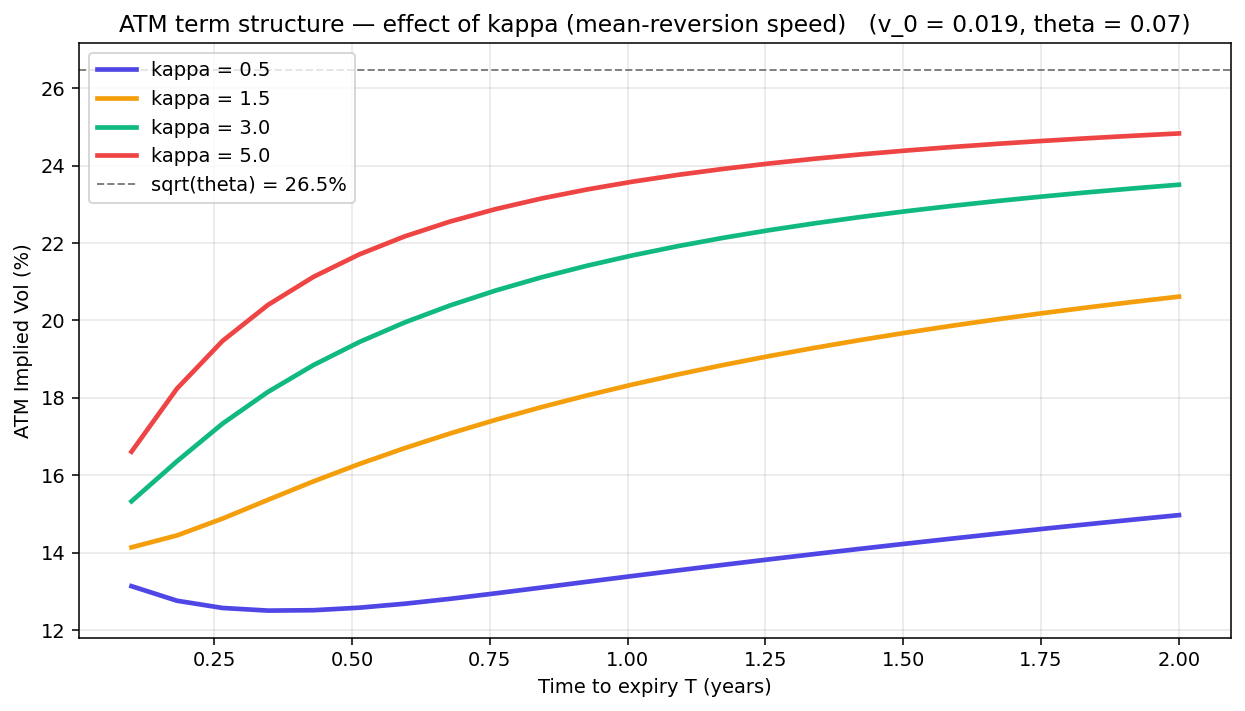

Switch axes. Instead of plotting a smile at fixed $T$, plot the ATM implied vol as a function of $T$. The shape is now a "term structure" — short-dated vol on the left, long-dated vol on the right. $\kappa$ controls how fast it converges to its long-run level $\sqrt{\theta}$.

High $\kappa$ snaps the term structure flat quickly. Low $\kappa$ leaves a long transient where the surface still remembers the starting variance $v_0$.

def atm_term_structure(maturities, **overrides):

ivs = np.full_like(maturities, np.nan, dtype=float)

for i, T in enumerate(maturities):

try:

ivs[i] = implied_vol(heston_call(S0, T, **overrides), S0, T)

except Exception:

pass

return ivs

Ts = np.linspace(0.1, 2.0, 24)

plt.figure(figsize=(9, 5.2))

for kappa_val in [0.5, 1.5, 3.0, 5.0]:

ivs = atm_term_structure(Ts, kappa=kappa_val)

plt.plot(Ts, ivs*100, lw=2.4, label=f"kappa = {kappa_val}")

plt.axhline(np.sqrt(THETA)*100, color="gray", ls="--",

label=f"sqrt(theta) = {np.sqrt(THETA)*100:.1f}%")

plt.title(f"ATM term structure — effect of kappa (v_0 = {V0}, theta = {THETA})")

plt.xlabel("Time to expiry T (years)"); plt.ylabel("ATM Implied Vol (%)")

plt.legend(); plt.grid(True); plt.tight_layout(); plt.show()

All four curves start from the same near-ATM short-dated vol and asymptote to $\sqrt{\theta}$. $\kappa = 5$ gets there fast; $\kappa = 0.5$ drags out the transition over the full 2-year window.

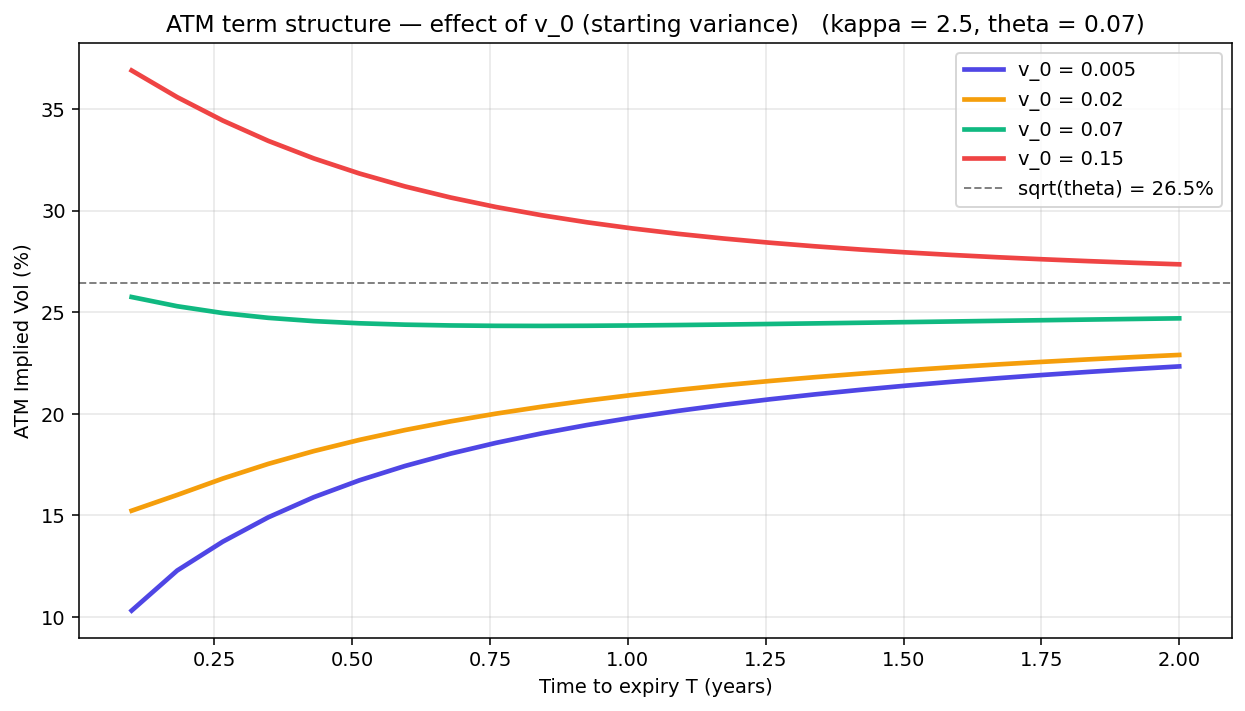

$v_0$ is "today's variance state". It's the only parameter on this page that's actually observed in the market (via short-dated ATM implied vol). Higher $v_0$ lifts the entire term structure; lower $v_0$ drops it. Both still mean-revert to $\sqrt{\theta}$ given enough time, just from a different starting point.

The reel at the top of this page animates $v_t$ along an SDE path. Each frame is a recomputed surface at the current $v_t$ — the breathing-up-and-down you see is exactly the four curves below shifting between regimes.

plt.figure(figsize=(9, 5.2))

for v0_val in [0.005, 0.02, 0.07, 0.15]:

ivs = atm_term_structure(Ts, v0=v0_val)

plt.plot(Ts, ivs*100, lw=2.4, label=f"v_0 = {v0_val}")

plt.axhline(np.sqrt(THETA)*100, color="gray", ls="--",

label=f"sqrt(theta) = {np.sqrt(THETA)*100:.1f}%")

plt.title(f"ATM term structure — effect of v_0 (kappa = {KAPPA}, theta = {THETA})")

plt.xlabel("Time to expiry T (years)"); plt.ylabel("ATM Implied Vol (%)")

plt.legend(); plt.grid(True); plt.tight_layout(); plt.show()

Fan-shape. Low starting variance ($v_0 = 0.005$, blue) climbs up to $\sqrt{\theta}$. High starting variance ($v_0 = 0.15$, red) decays down to the same level. The four curves cross only at the long end — that's the mean reversion of $v_t$ playing out.

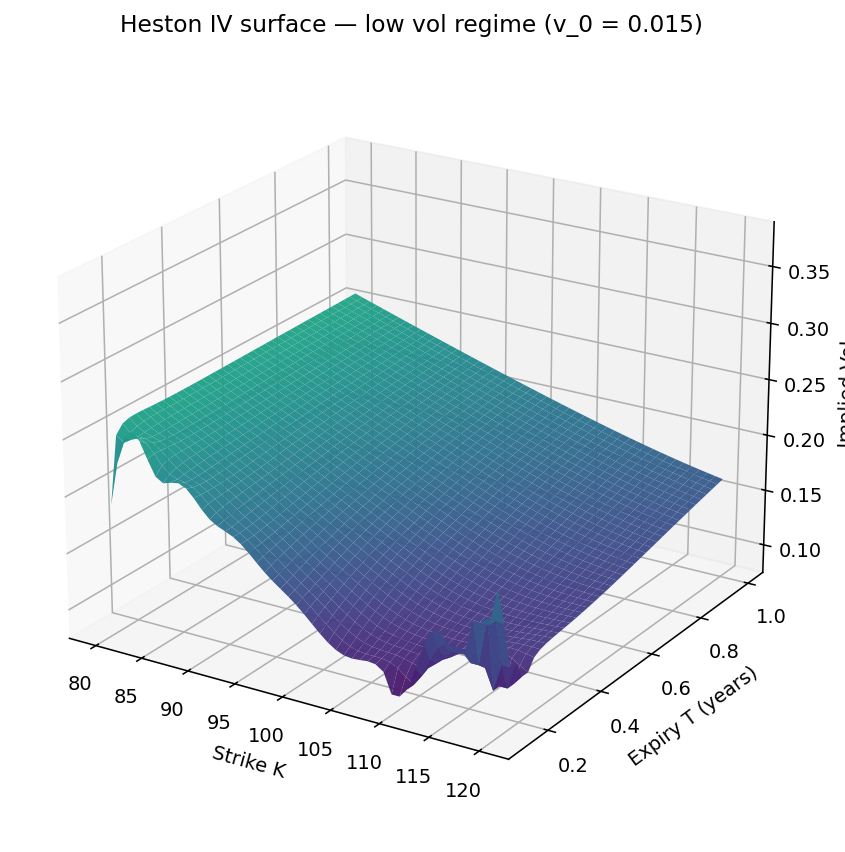

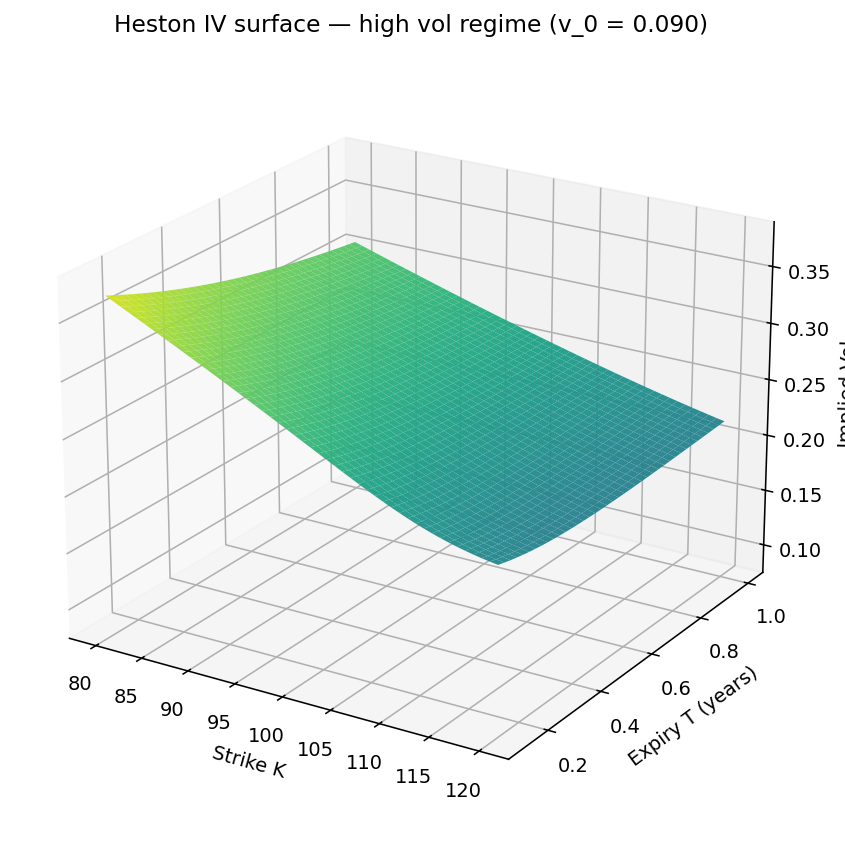

With the 1D slices in hand, the 3D surface is just $IV(K, T)$ on a grid. Strike on one floor axis, expiry on the other, implied vol as the height. To see how the surface morphs with the state, the trick (same as the gamma page) is to compare two snapshots on the same z-axis: a low-vol regime and a high-vol regime, identical otherwise.

from matplotlib import cm

strikes = np.linspace(80, 120, 50)

maturities = np.linspace(0.12, 1.0, 40)

K_mesh, T_mesh = np.meshgrid(strikes, maturities)

def full_iv_surface(v0_val):

iv = np.zeros_like(K_mesh)

for i, T in enumerate(maturities):

for j, K in enumerate(strikes):

try:

iv[i, j] = implied_vol(heston_call(K, T, v0=v0_val), K, T)

except Exception:

iv[i, j] = np.nan

return iv

iv_low = full_iv_surface(0.015) # low-vol regime

iv_high = full_iv_surface(0.090) # high-vol regime

z_max = max(iv_low.max(), iv_high.max()) * 1.05

z_min = min(iv_low.min(), iv_high.min()) * 0.85

for tag, iv, title in [

("low", iv_low, "Low vol regime (v_0 = 0.015)"),

("high", iv_high, "High vol regime (v_0 = 0.090)"),

]:

fig = plt.figure(figsize=(9, 6.2))

ax = fig.add_subplot(111, projection="3d")

ax.plot_surface(K_mesh, T_mesh, iv, cmap=cm.viridis, edgecolor="none",

alpha=0.95, vmin=z_min, vmax=z_max)

ax.set_zlim(z_min, z_max)

ax.set_title(f"Heston IV surface — {title}")

ax.set_xlabel("Strike K"); ax.set_ylabel("Expiry T (years)")

ax.set_zlabel("Implied Vol")

ax.view_init(elev=22, azim=-58)

plt.tight_layout(); plt.show()

$v_0 = 0.015$ (vol $\approx 12\%$). The surface sits in the bottom half of the cube, tilted left from $\rho = -0.72$. ATM IV climbs gently with $T$ as the model mean-reverts up to $\sqrt{\theta} \approx 26.5\%$.

Same z-axis. $v_0 = 0.090$ (vol $\approx 30\%$). The whole surface lifts upward — short-dated vol is now above the long-run level, and the term structure slopes down toward $\sqrt{\theta}$ as $T$ grows. Skew direction is preserved (rho hasn't changed), only the level.

Reading the dynamics off the two pictures:

Put together: Black-Scholes gives you a single point. Heston gives you a five-parameter surface that can match observed skew, smile curvature, and term structure — and one of those five parameters ($v_t$) actually evolves through time, which is why the surface breathes.

Pair this notebook with the Black-Scholes IV calculator, the gamma surface notebook, and the option Greeks notebook to see the same surface from different angles. Heston is the natural place to go after gamma — once you've stared at a BS surface long enough to feel the limits of the flat-vol assumption, the stochastic vol generalisation stops feeling like math and starts feeling like a fix for an honest gap in the model.

Everything on this page packaged as a runnable Jupyter notebook, plus content that didn't fit here. Join the newsletter (free) and the download is yours.

Write your name and a valid email to unlock the download.

heston_vol_surface_extras.ipynb

Enter your name & email above to unlock

Free. One short email when there's something new. No spam, unsubscribe in one click.